The Three Paths Money Takes in Life: Understanding the Journey from Poverty to Wealth

Money plays a significant role in shaping people's lives. It influences whether they stay stuck in poverty, live a comfortable middle-class life, or achieve financial freedom and wealth. Understanding how money moves through a person’s life is essential for anyone aiming to build wealth and financial security. This article explores the three distinct paths that money can take and how the choices made along these paths can determine one's financial future.

Introduction: Money’s Role in Shaping Lives

The way money moves in our lives is a key factor in determining our financial future. It’s not just about how much money we earn but also about how we handle it, invest it, and make it grow. Some people remain stuck in poverty, while others seem to move effortlessly into the middle class or even achieve great wealth. The journey money takes in a person's life follows a specific pattern—whether it ends in financial freedom or a life of struggle depends on the choices made along the way.

For many, personal finance journeys start with basic financial education. One of the most popular books that kickstarts this journey for many is Rich Dad, Poor Dad by Robert Kiyosaki. Although some concepts in the book may not fully apply to every country or culture, the fundamental lessons about money are universal. The book highlights how money moves in our lives and introduces the concept of three distinct financial paths. These paths, when understood, can help anyone avoid financial traps and build long-term wealth.

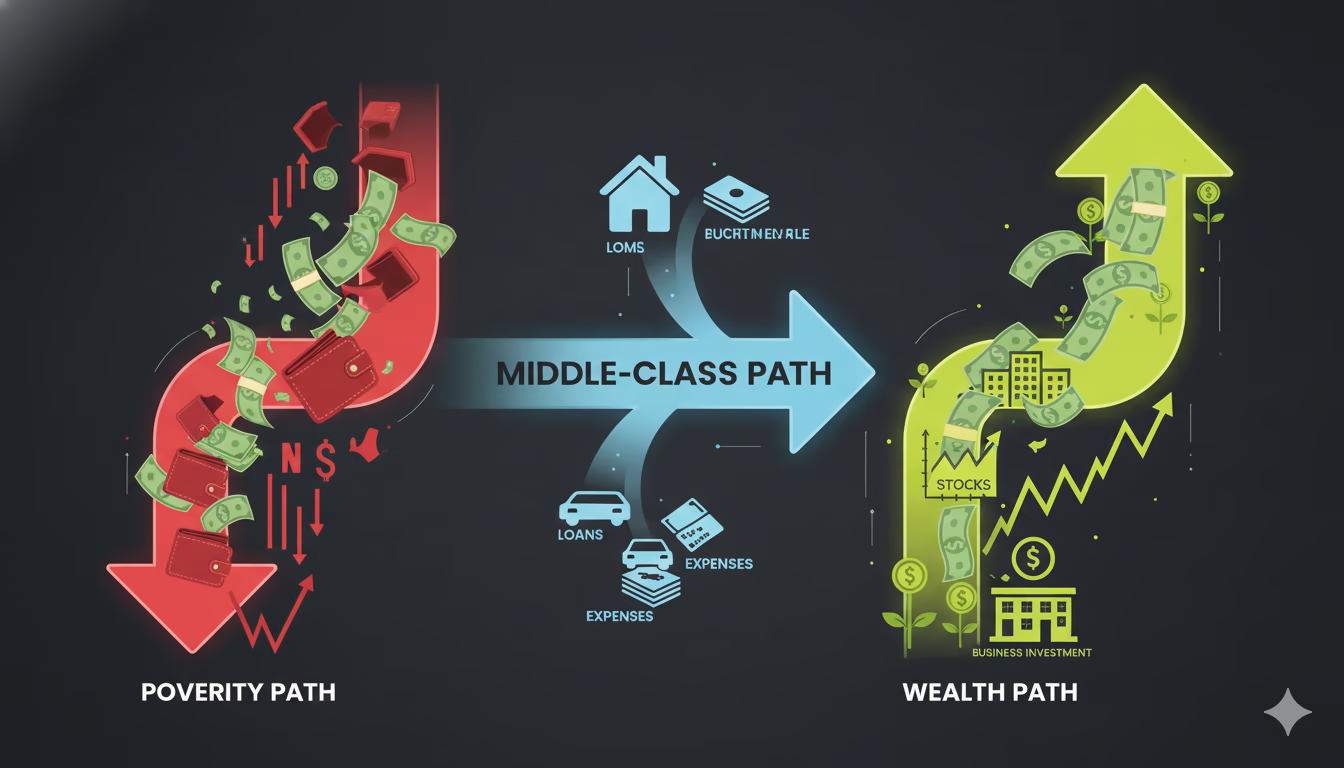

Path 1: The Poverty Path

The first path money can take in life is the "Poverty Path." This path is often characterized by an immediate outflow of money with little to no regard for saving or investing. Those on this path have a mindset that prevents them from making long-term financial decisions. Instead, they prioritize short-term wants over needs and long-term financial health.

Picture a person who earns a regular income, say $1,200 a month. They might spend all their money immediately, often on things they don’t need—luxuries such as dining out, expensive clothes, gadgets, or vacations. For them, money comes in, but it quickly vanishes. This lifestyle can create a cycle of financial instability, where no savings are built, no assets are accumulated, and no investments are made. Despite earning a decent amount, they remain financially insecure because they live paycheck to paycheck.

A critical element of the Poverty Path is the lack of financial education. These individuals often don’t understand the difference between assets and liabilities. They might purchase things like an expensive car or an oversized home, thinking they are "wealthy" because of their possessions. However, these items don't generate income and can lead to high expenses, keeping them trapped in a cycle of debt and poor financial habits.

The key takeaway from the Poverty Path is this: money flows out as quickly as it flows in. No matter how much one earns, if they don’t control their spending habits and prioritize building wealth, they will remain stuck in financial instability.

Path 2: The Middle-Class Path

The second path is the "Middle-Class Path," which is the most common financial trajectory for many people. In this path, money flows into one's life but is often channeled into buying things that provide a temporary illusion of wealth. People in this category might earn a steady income, buy a house, drive a nice car, and take vacations—but these purchases are often funded by loans or credit. While this path may appear successful on the outside, it hides the fact that many middle-class individuals are living with significant debt.

A common characteristic of the middle-class path is the idea of accumulating liabilities instead of assets. Liabilities are things that take money out of your pocket, such as a car loan, mortgage payments, or credit card debt. On the other hand, assets are things that put money into your pocket, such as rental property, stocks that pay dividends, or a side business that generates extra income.

For instance, a person might buy a home, but instead of it being a source of income, it’s a liability that requires constant payments for the mortgage, maintenance, and property taxes. Similarly, buying a car might make someone feel wealthy, but it is a depreciating asset that costs money to maintain.

The middle-class mindset tends to prioritize the outward appearance of wealth. People on this path often focus on acquiring things that boost their social status, but fail to invest in long-term assets that generate income. Over time, this can lead to a situation where people are trapped in a cycle of debt, paying for liabilities that drain their income. The Middle-Class Path might look comfortable, but it doesn’t necessarily lead to financial freedom.

Path 3: The Wealth Path (The Rich Path)

The third path, and the one that leads to true financial freedom, is the "Wealth Path" or "Rich Path." People who take this path focus on acquiring assets that generate income. The key difference between this path and the others is a shift in mindset: rather than spending money on liabilities or unnecessary wants, those on the Wealth Path invest in things that will increase their wealth over time.

The first principle of the Rich Path is to spend money wisely. Instead of buying things that depreciate in value or require ongoing payments, people on this path focus on investments that grow their wealth. This could include buying stocks, real estate that generates rental income, starting a business, or investing in skills that can lead to higher-paying opportunities in the future. The goal is to accumulate assets that produce passive income.

Once people on the Rich Path have accumulated a significant amount of assets, they can reinvest the income generated from those assets into more assets, further growing their wealth. For example, they might take the dividends from stocks or the rent from a property and use that money to buy more shares or properties. Over time, this compounding effect leads to greater financial freedom and wealth.

One of the most important lessons of the Rich Path is that people who achieve wealth focus on creating multiple streams of income. They don't rely solely on their job or one income source. Instead, they build diverse investments that provide returns from different channels. By doing so, they ensure that their wealth continues to grow even when their primary income source is not active.

How to Start Following the Wealth Path

Starting to follow the Wealth Path requires changing your mindset and making conscious decisions about how to manage your money. Here are some steps that anyone can take to begin building wealth:

- Track Every Expense: Understanding where your money goes is the first step to financial freedom. Categorize your expenses into needs, wants, liabilities, and assets. This will help you identify areas where you can cut back and invest more.

- Invest Regularly: Even small amounts of money can make a difference over time. Whether it’s setting up an automated investment plan or making regular contributions to a retirement account, consistency is key. Over time, even small investments can grow significantly.

- Shift Your Mindset: Move from an employee mindset to an investor mindset. Focus on multiplying your money rather than simply earning it. Be willing to take calculated risks and learn about the best ways to invest.

- Play the Long-Term Game: Wealth doesn’t happen overnight. The key to financial freedom is consistent, long-term investments. Be patient and stay committed to your goals.

- Surround Yourself with the Right People: Network with those who can challenge and inspire you. Learn from people who are financially successful and avoid those who encourage a lifestyle of constant consumption and debt.

- Develop Financial Intelligence: It’s not enough to simply be financially literate. To truly build wealth, you must understand how to make smart investment decisions, manage risk, and allocate money effectively.

Conclusion: Which Path Will You Take?

Money moves through three distinct paths: poverty, middle class, and wealth. While it’s important to acknowledge that not everyone has the same financial opportunities, understanding how money moves and how to control it is crucial for building long-term financial success. The Poverty Path keeps people stuck in a cycle of debt and consumption. The Middle-Class Path might offer comfort, but it can be a trap if it doesn’t include a focus on building wealth through assets. The Wealth Path, on the other hand, offers the potential for true financial freedom, provided that money is invested wisely and reinvested to grow wealth over time.

By shifting your mindset, focusing on building assets, and making informed financial decisions, you can start your journey toward financial freedom. The choice is yours: which path will your money take?